Netflix: A Case Study in Rational Investing Amid Uncertainty

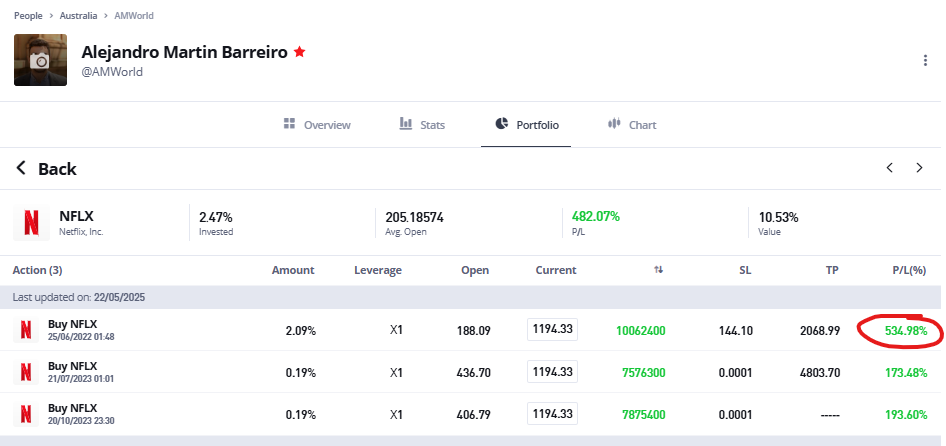

🎬 How I bought a hated stock in June 2022 and saw a 535% return

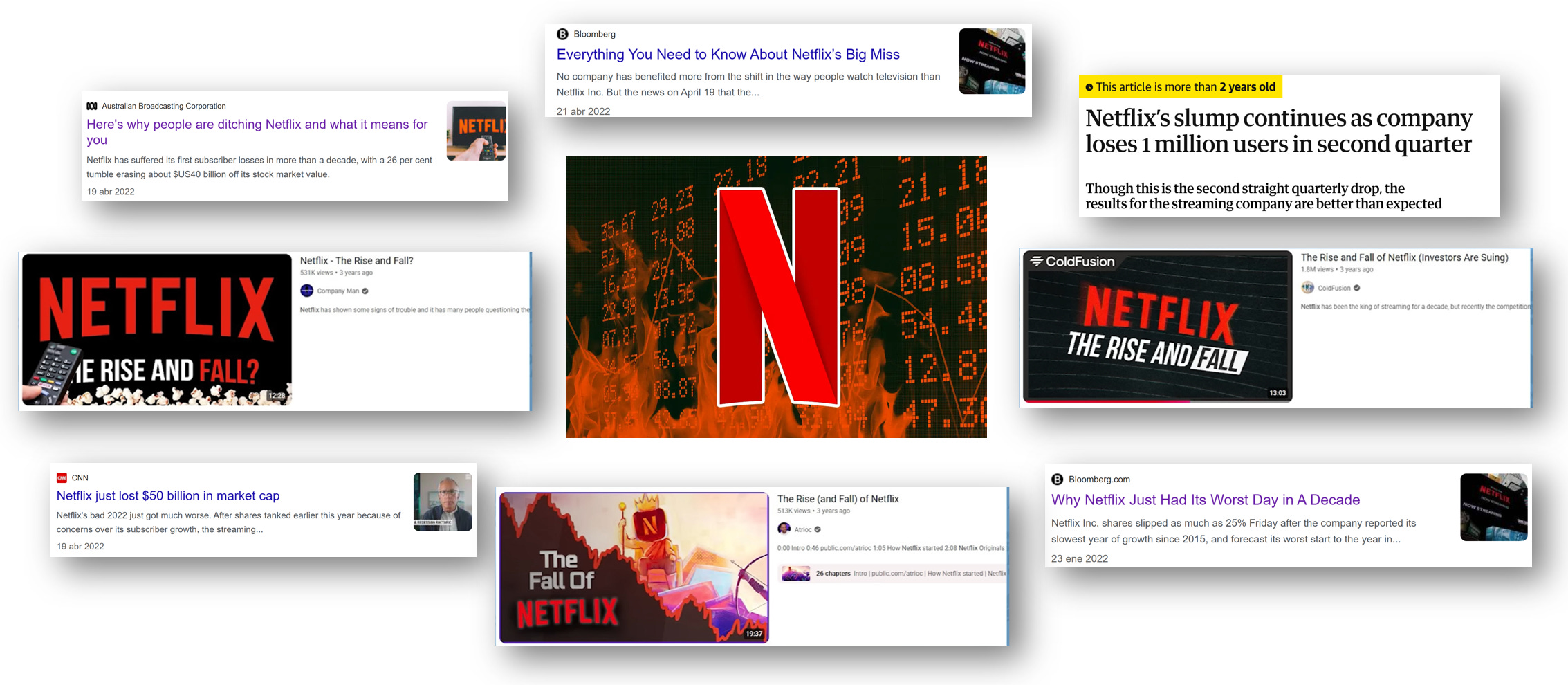

Introduction: Netflix down 70%

In June 2022, I added Netflix (NFLX) to my portfolio on eToro—right when most investors were fleeing. The stock had plummeted over 70% from its highs, sentiment was at rock bottom, and analysts were raising serious concerns about subscriber growth, competition, and saturation.

But what I saw was different.

I saw a company with a powerful business model, enduring moats, and the ability to adapt and emerge stronger. This post is a deep dive into why I invested in Netflix and how it fit my Value Growth Strategy. It’s a real example of how I apply my investment philosophy and checklist methodology to buy great companies in times of fear.

Key Highlights

Netflix returned +535% in my portfolio since purchase.

Bought during a time of maximum fear, after a 70%+ decline.

Fundamental analysis showed durable moats, pricing power, and adaptability.

Passed my checklist with high scores on fundamentals and technicals.

Growth outlook remains strong, especially in advertising, and gaming.

Here an screenshot of my position of NETFLIX in eToro:

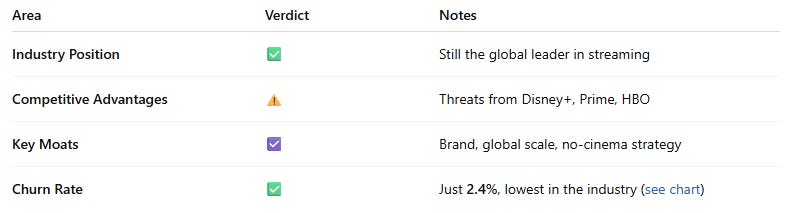

Business Model Overview

Netflix is the world’s leading streaming entertainment service, with 270M+ paid memberships globally. It offers content across multiple languages and genres, creating original and exclusive shows and films.

MOATs

Netflix has multiple durable competitive advantages:

Brand & Global Reach: The “Netflix” name is synonymous with streaming. With operations in 190+ countries, Netflix has scaled faster and deeper than its rivals.

Subscriber Loyalty: With a churn rate of just 2.4%, Netflix has the lowest cancellation rate among premium streaming services, far lower than Hulu’s 4.1% (see graph below). That signals deep user engagement and stickiness.

Content Production Scale: Its original content strategy and production capabilities are unmatched.

Unique Content: No Cinemas, No Distractions: Unlike Disney, which also monetizes via box office and merchandise, Netflix focuses solely on direct-to-streaming. That strategic clarity enhances operational efficiency and brand focus.

Data & Personalization: Its recommendation engine drives engagement and retention. Data and AI driven.

First Mover Advantage: Built infrastructure, global presence, and mindshare ahead of rivals.

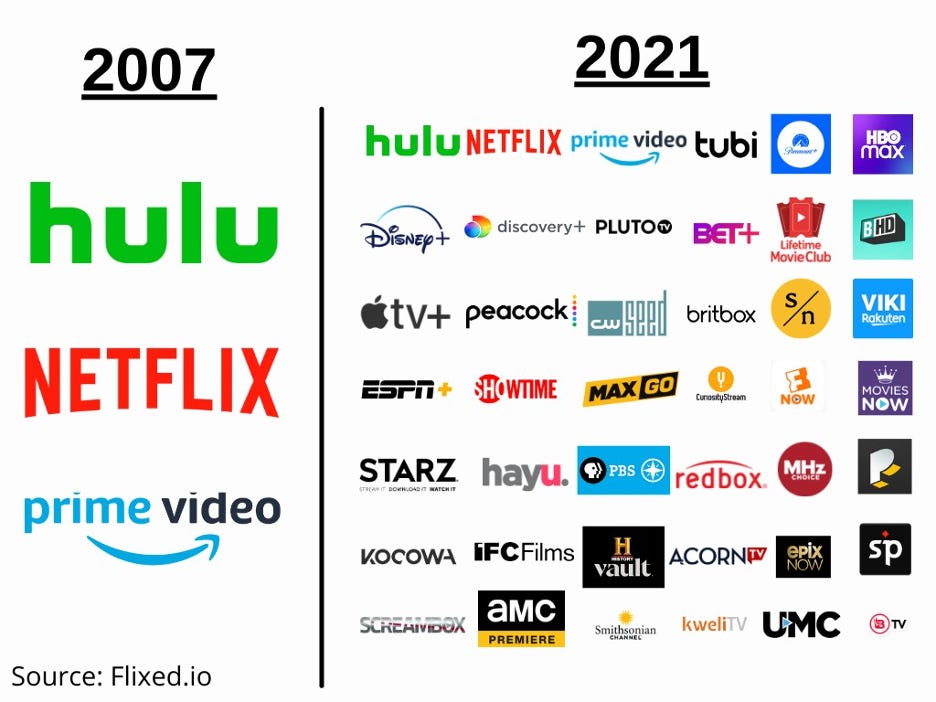

Competitors

Too Much Competition (June 2022): The "streaming war" narrative was everywhere. Disney+, HBO, Prime Video — all seemed poised to take market share. But most of them lacked Netflix’s combination of global scale, content library, and platform usability.

Netflix faces stiff competition—Disney+, Amazon Prime, Apple TV+, and YouTube—but none have replicated its focus + scale + profitability combo. Most operate streaming as a side business. Most of them canibalise their own business or spend lot of expenditure in advertisement or discounts. Netflix is all-in and has pricing power.

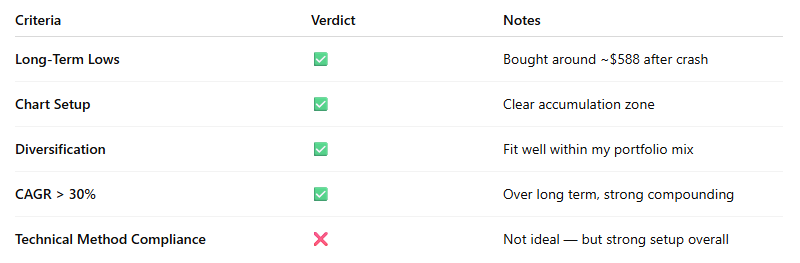

How Netflix Fit My Investment Checklist

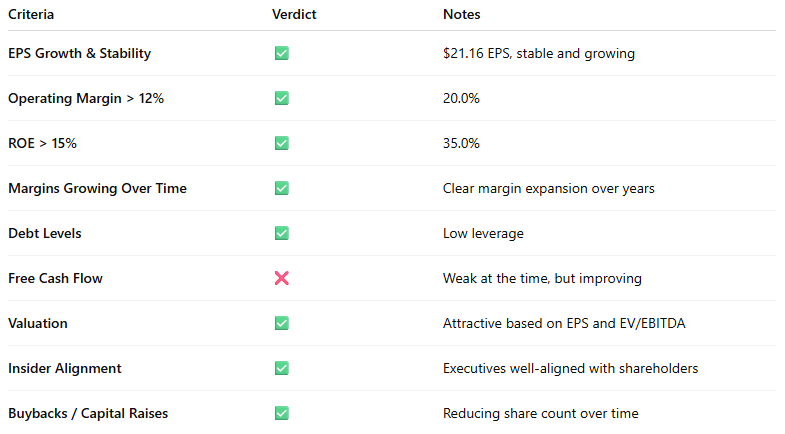

Before investing in Netflix in June 2022, I ran it through my Fundamentals and Technicals Checklist — a disciplined scoring system I use for every company. Netflix scored 74.55%, comfortably above my 70% threshold for long-term buy and hold.

Here’s how it performed across key areas:

🔹 Fundamentals (85% Weight)

Conclusion: Despite concerns, Netflix showed strong profitability, margin discipline, and shareholder-friendly behavior.

Moats & Competitive Edge

The moat analysis was more nuanced — strong engagement, but rising competition:

Netflix wasn’t a monopoly, but its brand loyalty, retention, and global reach created a moat hard to replicate.

Business & Sector

QuestionVerdictNotesUnderstandable Business Model✅Subscription-based streamingSector & Country Attractiveness✅US tech sector — scalable, high-growthCrisis Resilience✅Performed well in 2008, 2020, and adapted quickly post-COVID

The business model was simple, scalable, and proven across multiple crises.

Technicals (15% Weight)

Technically, the setup looked perfect:

The technicals showed panic selling, not fundamental collapse — creating a compelling entry point.

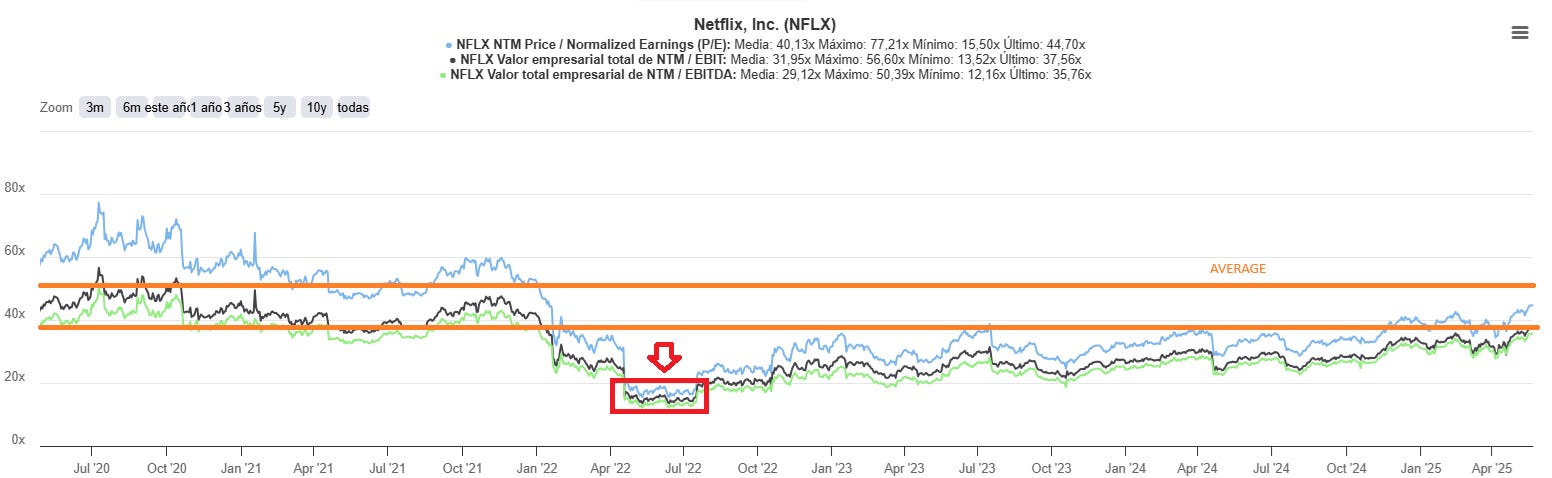

Valuation

05/2022: 3 Yeas ago Netflix was around 17x Forward P/E ratio, really below average.

05/2025: Now Netflix is around 44x Forward P/E ratio, aroun average (40x/50x)

Facing Our Fears

But even if everything looked good we needed to go through our fears, confront them in order to be confortable with the possible outcome.

🔻 Fears in 2021/2022

When we entered, the market was gripped by fear. Key concerns included:

Slowing subscriber growth, especially post-COVID. Zero Growth in Subscribers: Netflix reported flat or even negative subscriber growth in the previous quarters — sparking fears that the platform had peaked.

Our rational: Churn rate was lower and client retention was higher than competitors, the slow grow was due to the unsustainable expenditure in marketing by their competitors

Saturation in North America and Europe.

Our rational: Paid Ads and more Tiers while closing multiple ownership was an opportunity to increase revenue while giving more options to customers

High content costs and FCF negativity.

Our rational: Netflix was building great content and expanding into new regions what would allow for future strength thanks to engagement

Competitive pressure from Disney+, HBO Max, etc. Too Much Competition: The "streaming war" narrative was everywhere. Disney+, HBO, Prime Video — all seemed poised to take market share.

Our rational: Competitors were cannibalising themselves in their other verticals and revewnue streams (cinema, cable tv), and expending unsustainably in gaining marketshare, only a matter of time.

Sentiment collapse after poor earnings reports. Sentiment vs Reality: The emotional tone in markets was extreme. Netflix had dropped over 70% from its highs.

Our rational: But the business model, margins, and user base remained intact. Perfect Moment to buy.

Final Verdict

This was my final veredict at 2022.

Total Checklist Score: 75%

Decision: BUY

Biggest Risk: Transitioning from growth to profitability; high competition

Biggest Opportunity: Global leader with scale, adapting fast to new monetization models at a great valuation, with good margin and expectation of growth.

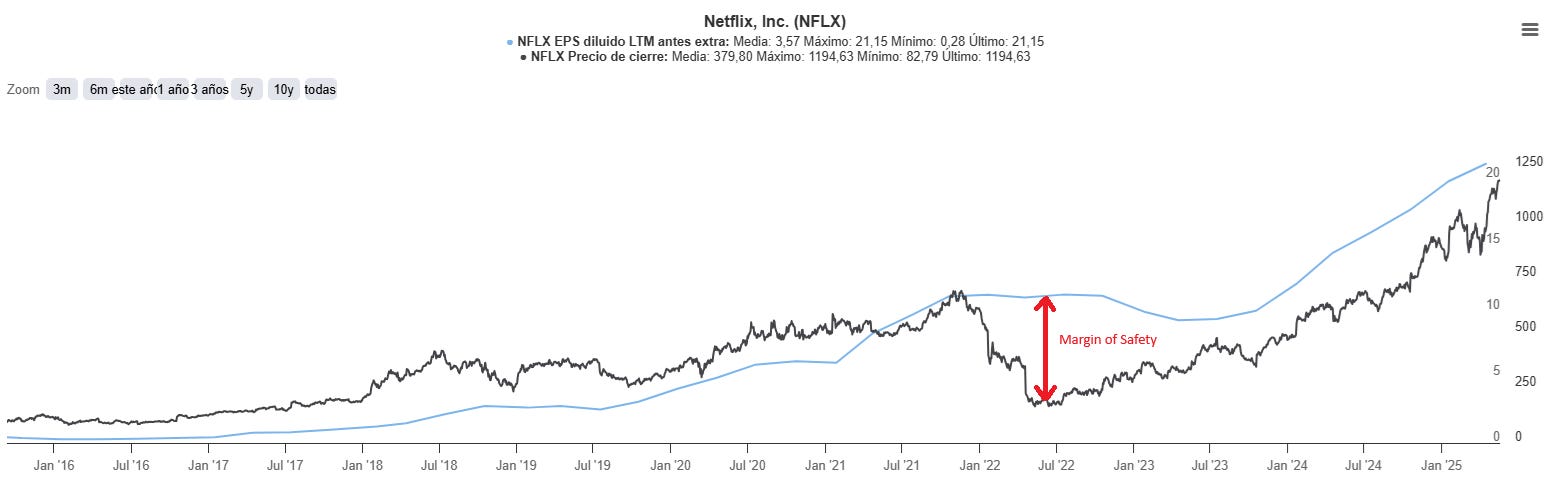

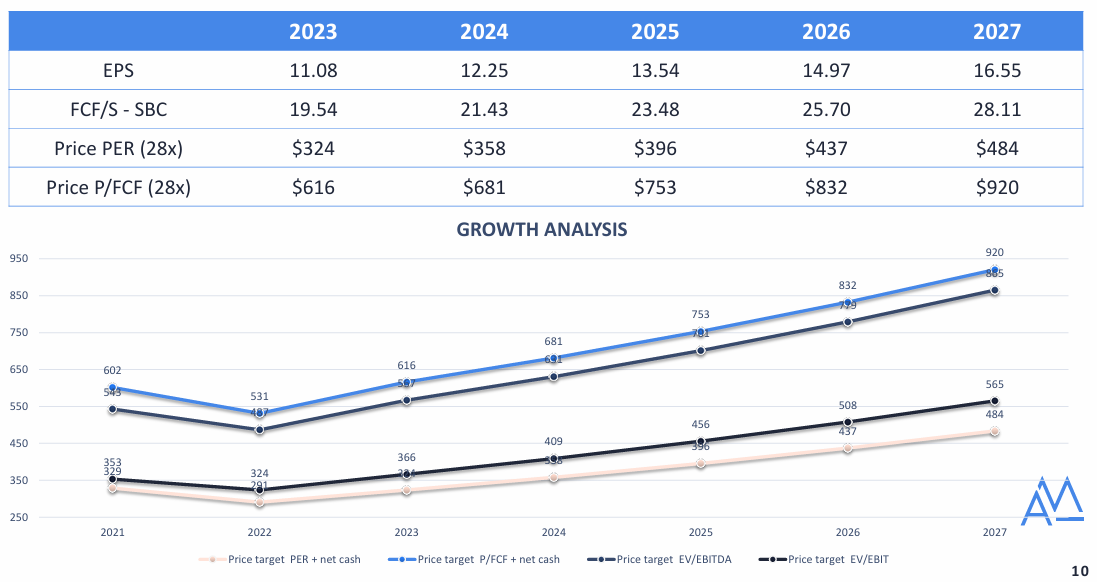

Here our Valuation and Price Forecast for NETFLIX at the time:

Netflix Outlook Today

Since our purchase, Netflix has not only recovered, it has transformed:

Successful launch of the ad-supported tier.

Cracked down on password sharing, boosting revenue.

Exploring gaming as the next frontier.

Developing their sports and events section

Continued international expansion.

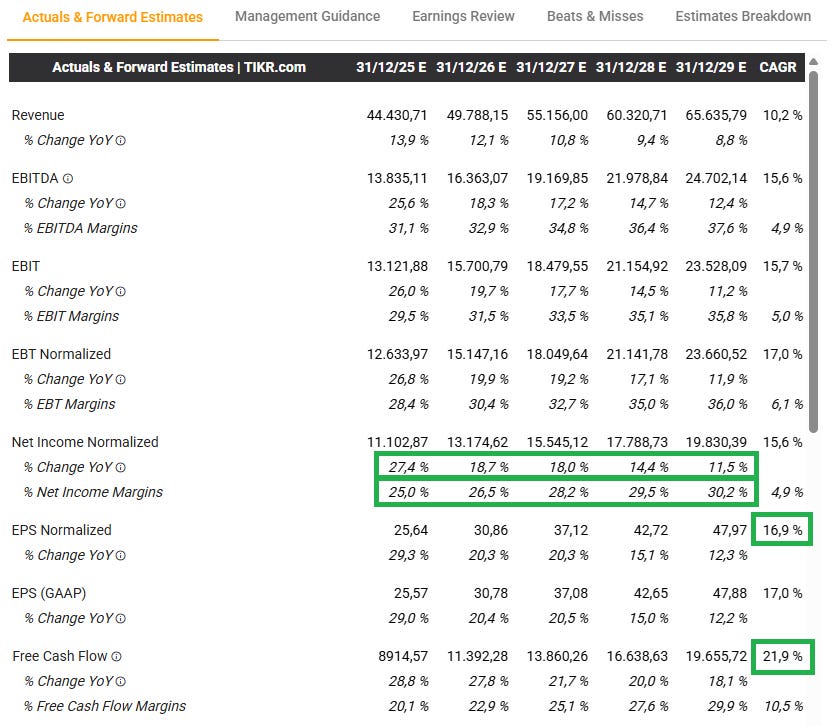

Now generating billions in free cash flow annually. Free Cashflow and Earnings per share to grow double digits.

Operating margin continues to expand as scale improves. It is expected margins will grow during the next years up +5%.

Conclusion

Netflix is a textbook case of what I look for: a Value Growth Stock with high-quality fundamentals, multiple moats, and a wide margin of safety. It passed my checklist when most were scared, and the return speaks for itself.

🧠 I’m not just writing about investing — I do it with my own money every day.

🚀 Want to invest like I do?

👉You can see my portfolio, follow me, or copy for free my investments on eToro.

🔎 No hype. Just smart, long-term investing in great companies at good prices

More stock breakdowns, investing lessons, and mindset posts coming soon. — make sure to subscribe to this Substack

Alejandro (AMWorld)

🌍 Popular Investor on eToro | Value Growth Strategy

📘 Disclaimer:

This content is for informational and educational purposes only. It is not financial advice, a personal recommendation, or an offer to buy or sell any financial product.

All views are my own and reflect my personal investment strategy. They do not consider your individual objectives or financial situation. Past performance is not a reliable indicator of future results. Investing involves risk — including the potential loss of capital.

I am a Popular Investor on eToro and may hold or trade positions in some of the assets mentioned. Some links may be affiliate or referral links, and I may receive a small compensation if you use them — at no extra cost to you.